Software is Back

Weekly Musing 05.09.26: Datadog, Twilio, and Atlassian crush the narrative

Are we turning the corner in software? I think so.

Q1 earnings season just handed us proof that the prevailing narrative about software was overblown. The reversal was violent.

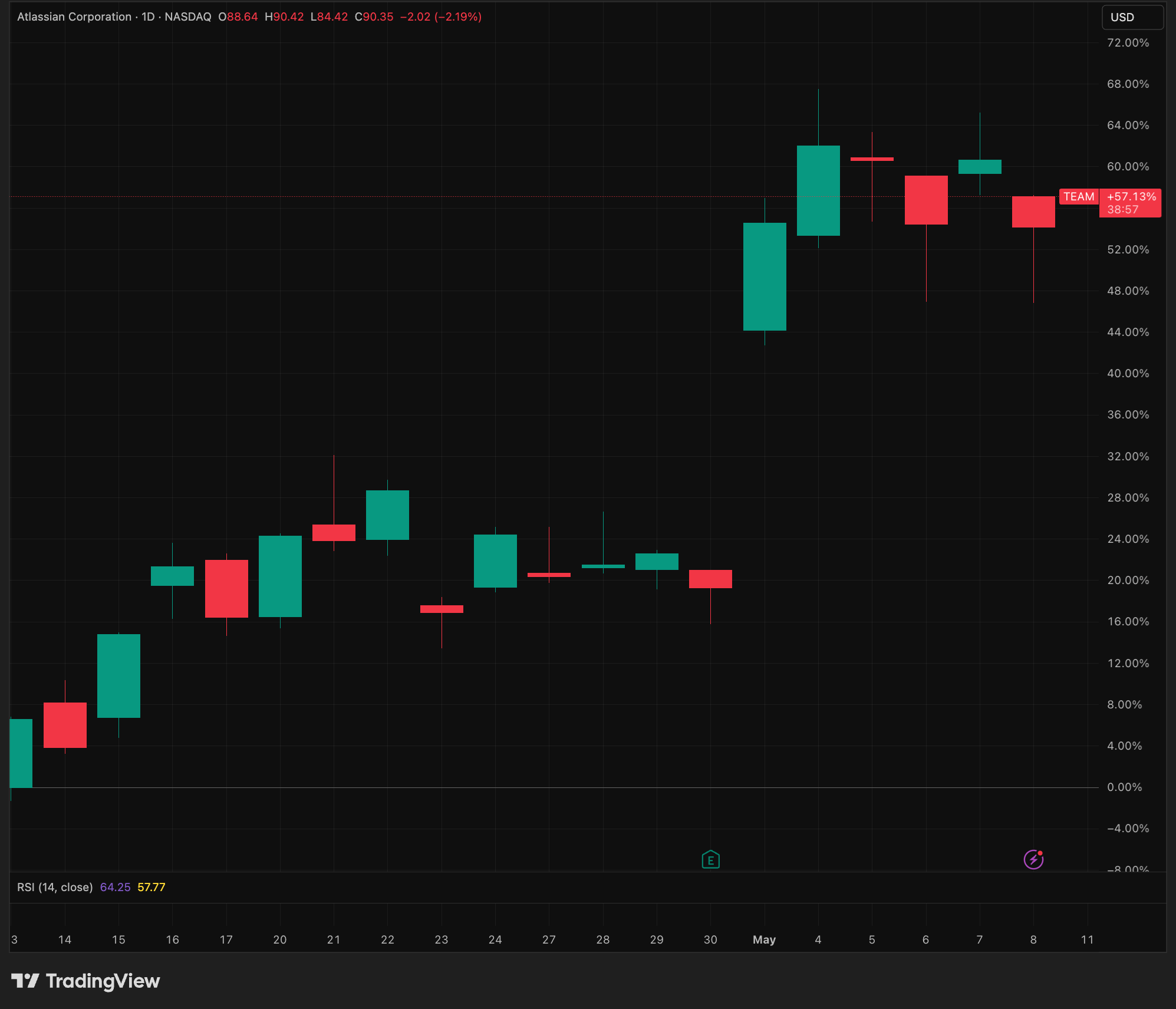

Atlassian (TEAM), the poster child of “AI can vibe code this,” is up almost 60% from lows and popped 30% on earnings.

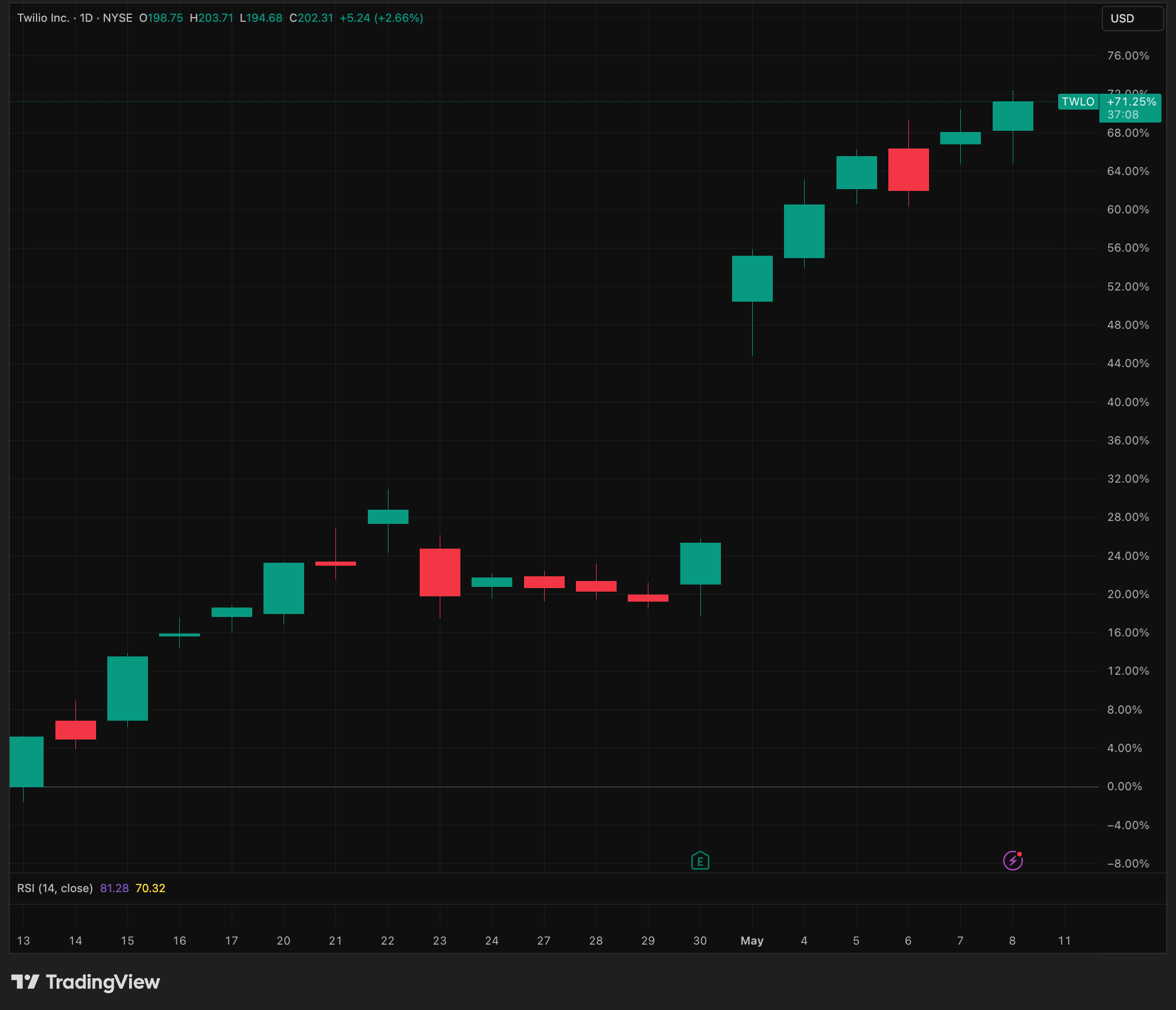

Twilio (TWLO) is up 70% from lows, and popped 24% on earnings announcement.

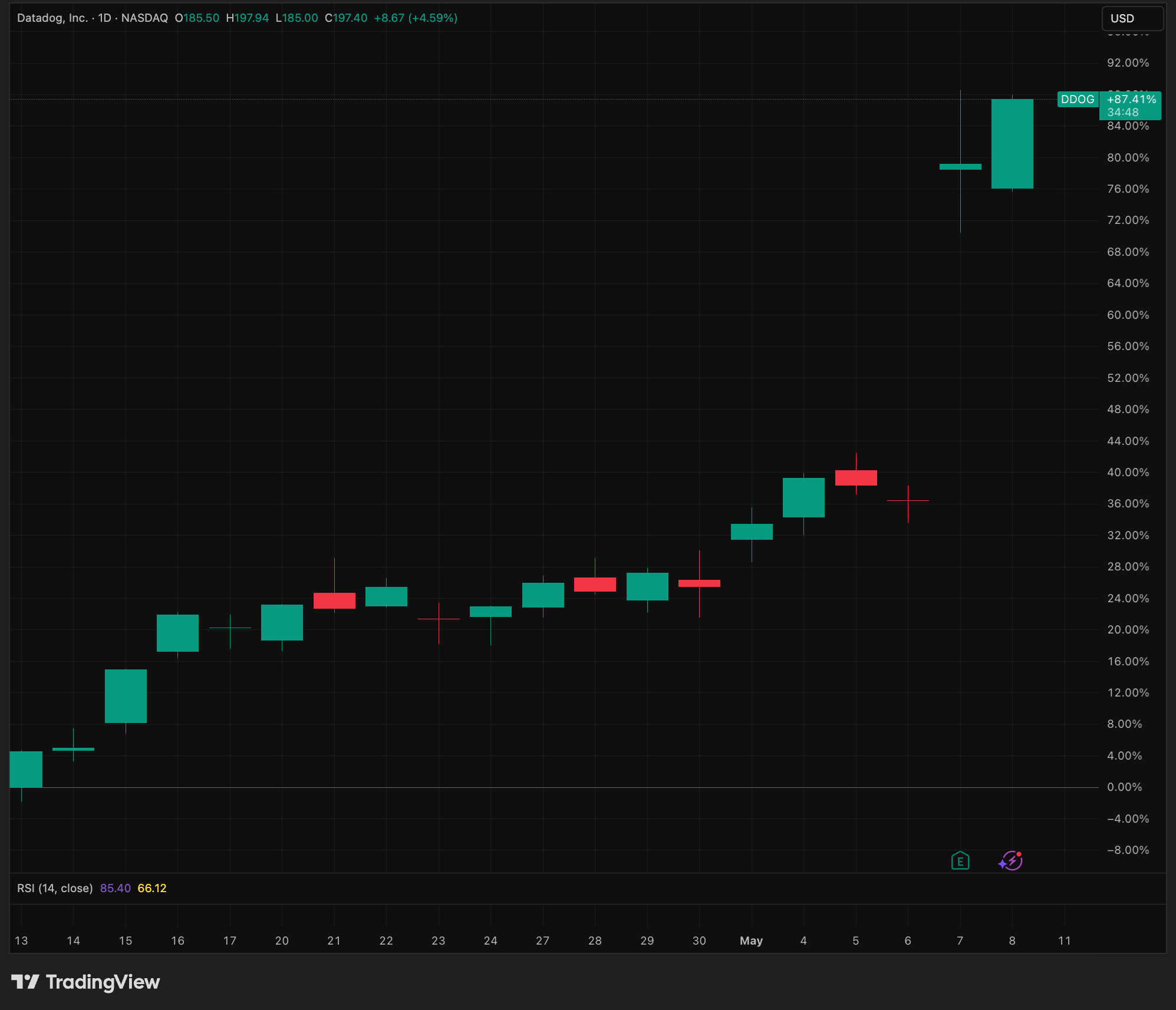

Datadog (DDOG) is up 87% from lows, and jumped 31% on earnings.

In the past few months, narratives drove markets. We saw a lot of hot takes. The cost to develop software is zero, so what advantages does an incumbent software vendor have? AI will replace people so companies won’t need to pay for seat licenses. The SaaS business model is dead.

Obviously, these takes were premature. I wrote a lot about this. My view was don’t generalize. The blast radius is uneven.

Q1 earnings showed early winners

Datadog accelerated revenue growth to +32% this quarter. The company prints in pure consumption — you spin up more workloads, the meter runs faster. Read more in my earnings note below.

I also wrote about why observability becomes more critical as agentic workloads multiply.

The gist — agents write and ship orders of magnitude more production code than humans. This is more products and services that need to be monitored. Moreover, agents are doing a lot more than humans. They make many API calls, spawn subprocesses, hit databases, fail in weird ways, retry at unpredictable rates. An agent doing a thousand things per hour needs to be watched constantly. More agents = more Datadog.

Twilio is seeing agentic consumption come through in their messaging and telephony rails. Their revenue accelerated to +20% in Q1, up from just 11% last year. This one is less flashy than Datadog but the logic is clean: every agent that does something in the real world — books an appointment, sends a confirmation, fires off an alert — has to communicate through infrastructure someone owns. Twilio is the plumbing.

Atlassian had an impressive quarter driven by AI usage, and the story here is the most interesting of the three. They accelerated revenue growth to +32%, up from low 20s. Two distinct vectors are running simultaneously. First: their own agent, Rovo, is being bundled into product packages to drive adoption. Second: external agents — Cursor, Claude, tools like this one — increasingly need their own Atlassian licenses to interact Atlassian’s products. Jira tickets get created. Confluence pages get written. Bitbucket gets touched. Every agent that does development work is potentially a seat that needs to be licensed.

I will note that the bundling piece deserves a flag: Atlassian pulled some packaging creativity to get Rovo usage up, which means the numbers need to be read with some care. The real test isn't whether customers adopted it when it was handed to them — it's whether they run out of usage and expand. That answer will come in the next few quarters.

But the common thread is undeniable. All three companies saw real, measurable acceleration. All three are somehow connected to increased agentic activity. An agent managing your Jira backlog needs to get into your an Atlassian instance. An agent monitoring your infrastructure logs Datadog events. An agent doing customer service needs Twilio’s messaging rails. As agents use more services and get more work done, the meter runs and software vendors capture a portion of the productivity gains.

How to pick the winners?

Not every software company benefits equally. This is a point I’ve made before and the same one I keep stress-testing as evidence comes in. The characteristics that matter:

Consumption-native business model. If your revenue is already metered — you charge per API call, per event, per GB — then agents are just another source of consumption. The meter runs the same way. You don't need to renegotiate contracts or change your pricing architecture. You just watch the number go up. This is DDOG, SNOW, TWLO. Best positioned.

Seat-to-consumption transition. You have a legacy seat model but you're smart enough to build a consumption layer on top of it. Atlassian is doing this with Rovo bundling. Microsoft is doing this with GitHub Copilot shifting to seat+consumption pricing in June. It can work, but it requires packaging creativity, and the transition period requires careful change management. You also have to demonstrate that the consumption is actually driving some productivity gains. We are going to see more company try to make this jump, but not all of them will be successful.

Leadership quality. Founder-led or technically led companies have an advantage. Product velocity matters enormously in this environment. You need a leader who will ship. And successful, founder led companies have the battle scars / lived experiences to change and adapt.

Other names worth watching

Three more names that fit the framework, in varying degrees:

Snowflake (SNOW). The original consumption compounder. Data platforms have become the strategic backbone of enterprise AI — you can't make AI useful without a unified data layer. Sridhar has turned product velocity back on. They have nine-figure partnerships with Anthropic and OpenAI baked into the platform. Cortex Code, their agentic harness, just launched. The same factors that drove extreme growth in agentic coding apply to agents writing scripts to query data.

Akamai (AKAM). Hat tip to Citrini Research for putting this on my radar. Edge compute infrastructure plus active investment in edge inference for low-latency agentic workloads. Less obvious than the names above, but the logic is similar. If you own the edge, and agents increasingly need to run at the edge, you're sitting on something. They just reported earnings. And while current numbers aren’t amazing, they are signing billion dollar agreements with AI labs to handle their edge inference workloads. Revenue from these deals are expected to hit later this year. The stock is up 26% after earnings.

Docusign (DOCU). Another hated software name that is fundamentally misunderstood. Docusign wants to be more than digital contract signing. They want to own the entire contract lifecycle thorough their Intelligent Agreement Management platform — drafting, redlining, negotiation, execution. All of this is done manually today and take a lot of administrative hours. Contracting is squarely within scope where agents are best suited for. But there’s more. The cherry on top is Docusign’s repository of 100M customer agreement to train their own models on. This is a data advantage. IAM has grown from 0 to $350M ARR, or 11% of total, in 2 years, and is expected to grow 80% through the end of FY27.

Where will the budget come from?

What does productivity gain actually mean? Software companies are pretty unapologetic about it. They are coming after headcount budgets. It’s no surprise that every AI startup frames their TAM in investor pitches as global wages (i.e., trillions).

We might be seeing this disruption take place today. AI native startups are producing unprecedented amounts of revenue per employee, somewhere between $5-10M per employee. The leading tech company produce ~$2-3M per employee at best. Big companies are likely to become smaller, with many announcing hiring freeze and rolling layoffs. Orgs flatten, roles consolidate, and expectations increase.

In other cases, companies are aggressively hiring because they figure they can grow much more and take share. Datadog is putting its foot on the gas for R&D investment because they see an enormous TAM.

We’re also seeing company formation increase. Agents are reducing the barrier to get started. Founders are starting with a more lean mindset and leaning on more AI.

Whatever the case, software sees their value capture as a piece of productivity pie. Anthropic reportedly crossed $10B run rate at the start of this year and accelerated toward $44B ARR through April! That is a staggering amount of AI consumption. That spend has to route through infrastructure somewhere. Some of it goes to hyperscalers. Some of it goes to observability. Some of it goes to developer tools.

Portfolio update

Since my last update, a lot has happened and my portfolio has hit all time highs, up 36% YTD. Here where it stands: