Weekly Musing 03.06.26

Signs of bottoming, geopolitics, AI economic debate, manufacturing waking up

⏮️ LOOKING BACK

Markets at a Glance

The S&P 500 has gone sideways since November. Investors have been rotating sectors, keeping the overall index flat. But we are starting to see signs of some battered areas showing strength.

Software (IGV) has been up 8 straight days, despite a volatile ride in markets this week. Is this the bottom?

Bitcoin is also showing some strength, after a painful 6 months. Can it stick?

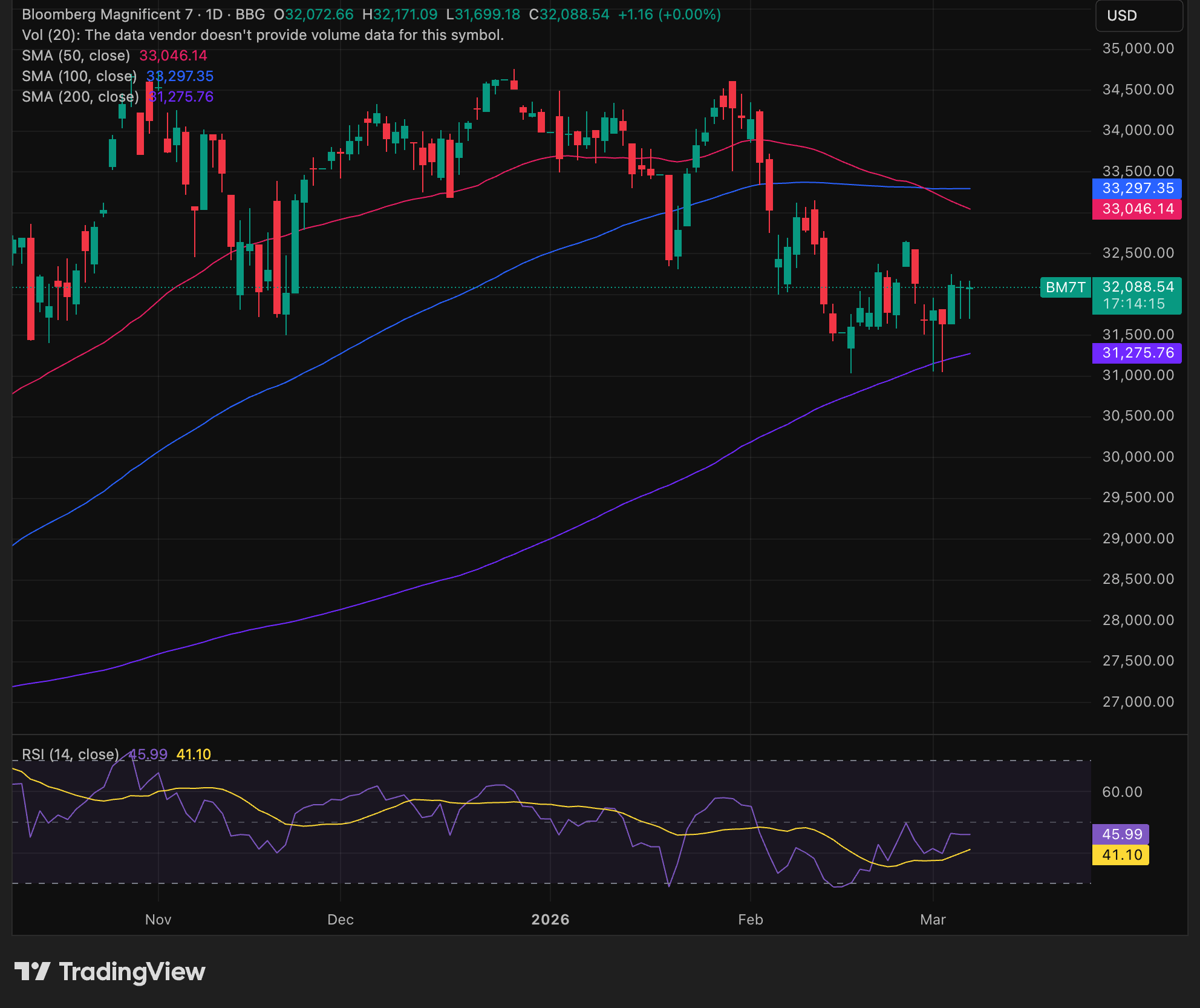

And the Magnificent 7 is bouncing off its 200 day moving averge.

Through the Strait

It’s been only a week since the beginning of the military campaign in Iran and global markets are starting to price a prolonged war.

The Strait of Hormuz is the chokepoint. A meaningful percentage of global oil, natural gas, and inputs for fertilizer flow through here. Ships paused transit after insurers pulled coverage due to elevated risk.

US stepped in to backstop insurance and provide Navy escorts. Oil prices eased on the news, but expectations of longer conflict in the region sent oil higher again to $80+.

The fertilizer angle might be under appreciated. Spring planting in the northern hemisphere is imminent. Supply disruptions in fertilizer inputs from the middle east could ripple into corn, wheat, and other prices over the next 6-12 months.

Asia and Europe are particularly vulnerable, as they depend on energy from the middle east. Korean and Japanese markets tumbled this week.

A prolonged war would be stagflationary. Commodity prices go up, government spends more on the military, potentially diverting resources from domestic growth.

My take: Things are changing quickly, but the market went from thinking this would be a contained conflict to now something that might very well become an ongoing war. This is a new inflationary pressure that would affect a bunch of stuff, including interest rates.

AI economic debate

If you haven't read Citrini's piece on AI and its macro implications, go do that first. Then read Citadel's rebuttal. This is one of the best intellectual debates happening in markets right now.

The core disagreement:

Citrini: AI will diffuse exponentially and quickly, create mass white collar unemployment, destroy aggregate demand, and cause a GDP collapse

Citadel: AI follows an S-curve (like every other technology), productivity booms are net positive, and the doom scenario violates basic “accounting identities”

Where Citadel lands punches:

The S-curve argument is strong: after rapid adoption, you hit diminishing returns as the “marginal adopter is less productive or less profitable which causes growth to decelerate.” This has been the pattern of technological innovation and economic impact historically.

Citadel believes AI will drive a productivity boom, resulting in real wage growth driven by falling prices (because AI will create more competition).

They go further to refute Citrini’s prediction of a wage spiral and GDP contraction. “A scenario in which productivity surges but aggregate demand (caused by wages decline) collapses while measured output rises violates accounting identities.” In other words, if wages fall, increased productivity will be redistributed through companies reinvesting (creating more work) or taxes (government).

Some thoughts:

Is globalization the right analogy? We did get cheap goods from abroad that raised our purchasing power. We also hollowed out the Rust Belt. The aggregate growth numbers looked fine, but the distributional effects were not. The assumption was the labor force would transition. It did, but not without casualties. And you could argue that has contributed, in part, to the political climate for the last 15 years.

So the question here is can society adapt fast enough to have a clean transition?

Side note: Citadel admitting that wealth redistribution through taxes would be necessary was not on my 2026 bingo card.

Earnings

Broadcom’s AI revenue is accelerating. They signed a sixth custom ASICs customer and signaled a lot of confidence for the next couple of years. Read more below.

Nvidia smashed earnings, in my opinion. Their latest generation chips delivered the goods and demand is broadening beyond the top 5 hyperscalers. Read more below.

Snowflake beat expectations and delivered impressive RPO growth, but the guidance for the year implies a growth deceleration. Sandbagging? Read more below.

Macro: Manufacturing is waking up

Feb ISM Mfg printed above 50 for the second consecutive month (hasn’t happened in a long time). Is the start to a a manufacturing expansion?

ISM Mfg Survey: 52.4 vs. 51.5 est. & 52.6 prior

New orders 55.8 vs. 57.1 prior

Prices paid 70.5 vs. 59 prior

Jan PPI came in hot

January PPI +2.9% vs. est.+2.6 & +3% prior

ex food and energy +3.6% vs. est. +3% & +3.3% prior

⏭️ LOOKING FORWARD

Macro:

We see jobs numbers for February today. Estimates have a meaninful slowdown in job adds MoM (130K → 58K) and a flat unemployment rate (4.3%)

Retail sales also come out today.

CPI / PCE come out next week. Both won’t reflect an recent moves in oil prices.

Energy may become more precarious, especially in Asia. I’m looking for any intervention to ease supply constraints. I’ll also be looking out for any spillover effects from a more prolonged conflict.

I’ll be watching software and crypto closely. If they continue to rally, we may have cleared the lows.

The only earnings on my radar for next week is Oracle.