Weekly Musing 03.13.26

Oil prices surging, TACO, USDC showing life

⏮️ LOOKING BACK

👀 Markets at a Glance

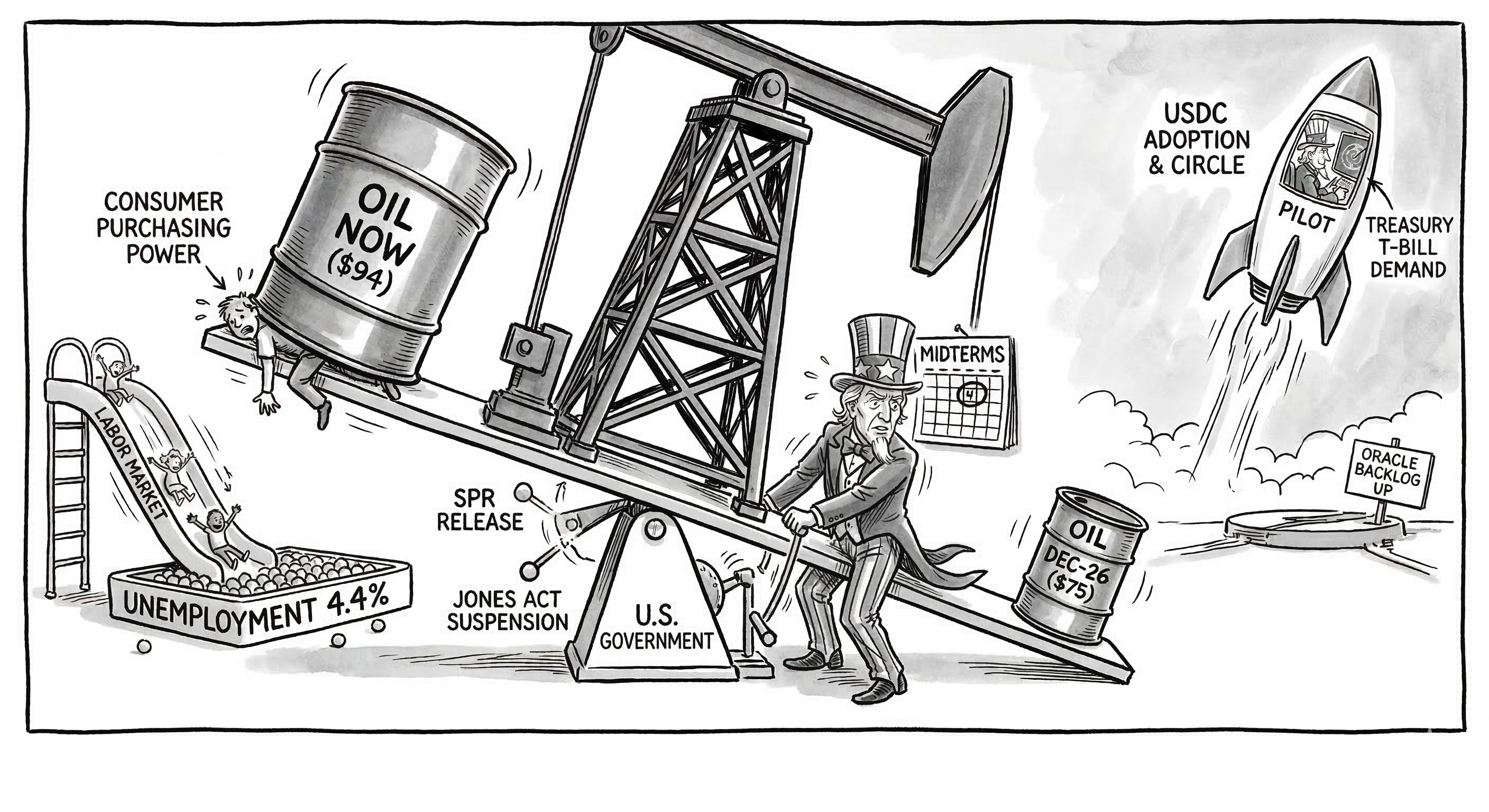

Since the conflict in Iran began, oil prices have surged ~45%, creating a massive ripple effect across global markets.

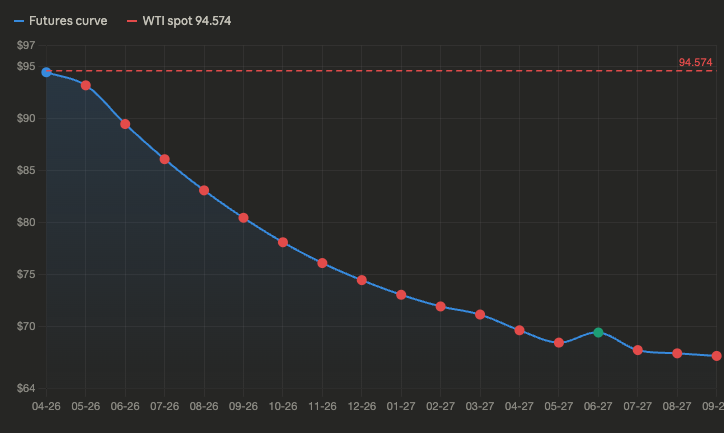

However, oil futures have not risen as much. Usually, oil markets exist in contango, where buying oil for future delivery costs a bit more than buying it today (to cover the cost of storing it). Right now, the market has flipped into extreme backwardation, meaning that oil right now is worth much more than in the future.

The price of a barrel delivered in December 2026 is just $75, 20% less the spot price of $94 at the time of this writing. This is the market pricing de-escalation or some sort of policy response.

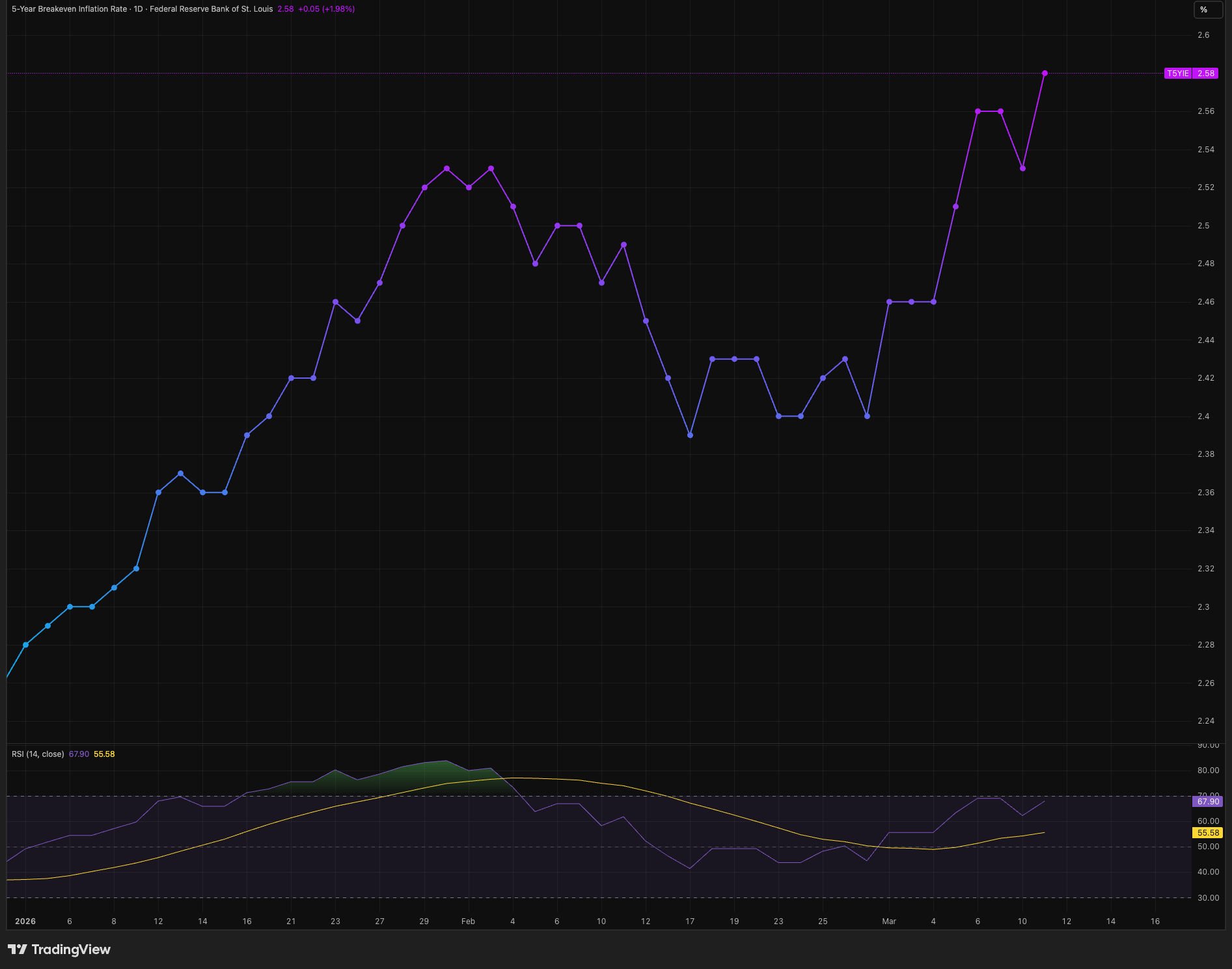

The first order effect of higher oil prices is an increase in inflation expectations. The 5-year break even rates is spiking.

Retail (XRT) and Consumer Discretionary (XLY) were among the sectors hit the hardest because inflation reduces purchasing power.

🌮 Markets expecting TACO

Markets are expecting another TACO move, predicting that Trump will call off the campaign in Iran. Domestically, Trump has to worry about the midterms, affordability, weakening labor markets, etc.

But the administration is reaching for it’s policy toolkit, which signals that campaign could go longer than anyone expected.

The administration released 172 of the 400+ millions of barrels in strategic petroleum reserve (SPR). This would release ~4m barrels a day for 40+ days.

They are weighing the suspension of the Jones Act, a 1920s era rule that requires US vessels to transport goods between its ports.

This would help balance supply and demand of oil throughout the country.

Some analyst speculate this could be a precursor to oil export controls. In this scenario, oil prices would fall domestically and rise everywhere else.

Gulf countries are also doing their part. Saudi Arabia and UAE are rerouting ~7 million barrels per day through pipelines built exactly for this purpose.

My take: Though things can turn on a dime, these moves would indicate that we are preparing for a longer siege in the Strait of Hormuz. The good news (so far) is that no permanent damage has been done to infrastructure.

At some point, Trump will have to face the political reality. But that doesn’t mean the temperature won’t turn up before then.

🚀 Stablecoin adoption taking off?

A few things have piqued my attention on stablecoins recently.

First, if you haven’t read my primer, here it is.

Here is what I’ve been noticing:

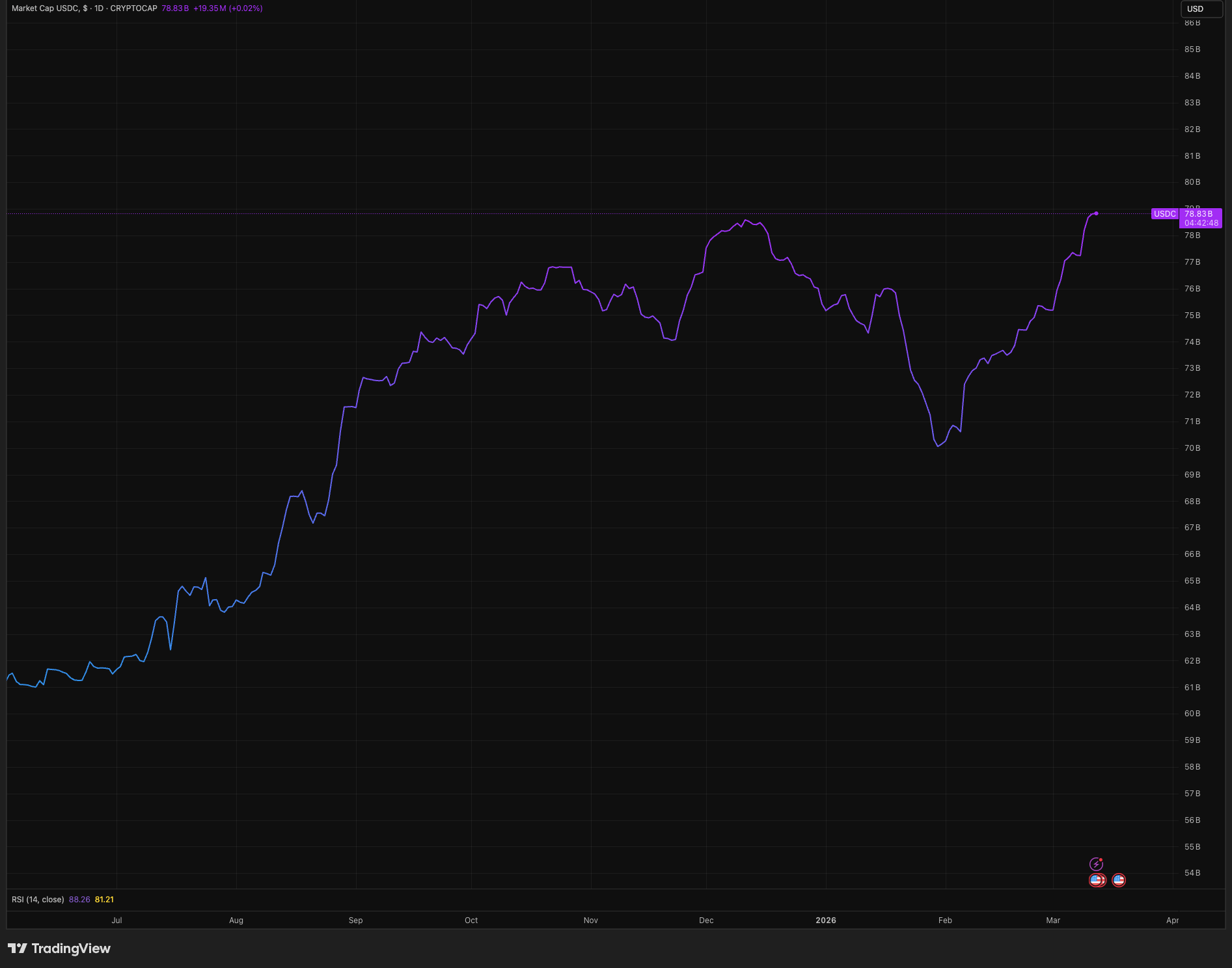

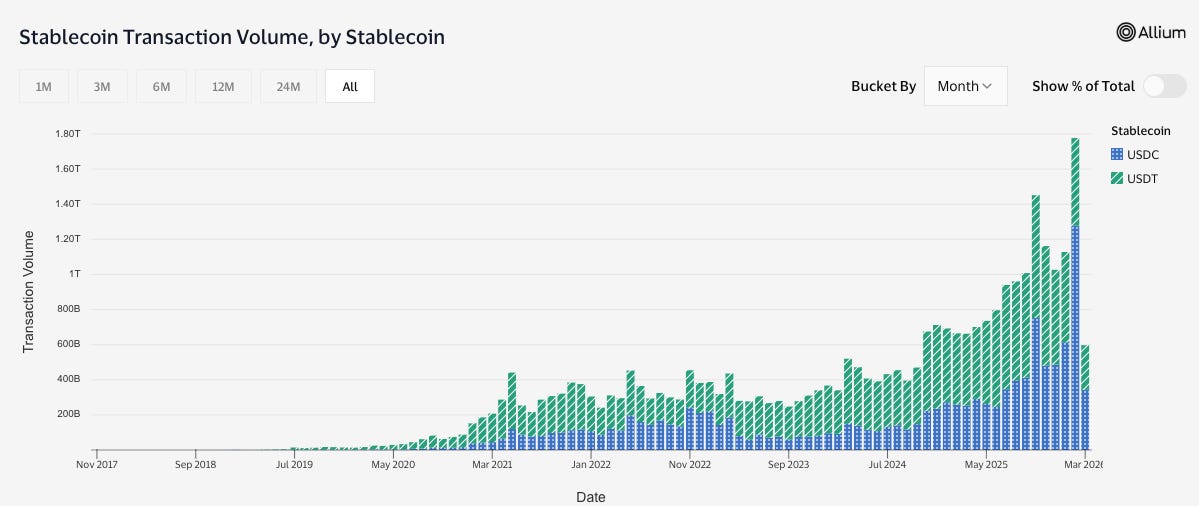

Circulation of USDC is surging, up 11% to $78B, since the beginning of February.

USDC transaction volume is also surging, overtaking the king, USDT (Tether). USDT is 2x the amount in circulation, so this is notable.

Circle’s stock (CRCL) has been going parabolic. They had a really good earnings print, but the momentum beyond that feels like something else.

My take: It’s been widely publicized that stablecoins will be a new tool for the Treasury department. If you want to understand this more, read my article above. The gist: Treasury needs a new price insensitive buyer for T-bills to finance the deficit and stablecoins play that role. This is a form of financial repression to keep rates low. The question was when will it start? Maybe soon.

Tangentially, on April 1st, new bank deregulation rules will take effect, relaxing eSLR requirements (here is a claude generated explanation). Without getting into the detail, the effect could unlock trillions in demand for treasuries (another form of financial repression). So makes sense that these two forms of financial repression would kick in at the same time.

Lastly, the Clarity Act is expected to get through Congress in the near-future (or that is the administration’s hope, at least). After passed, there would be no regulatory hurdles for the tokenized asset ecosystems to develop.

These are very early moves in what could be an inflection in stablecoin and tokenized asset adoption. I’ll be watching very closely.

Surging USDC circulation:

USDC transaction volume spiking, overtaking USDT:

Circle: green bars for days, surpassing moving averages.

Earnings

Oracle had a solid print, beating expectations. They also increased their backlog by $29B quarter over quarter. The stock moved up 10%. Read more below.

Macro: Weak jobs

🛑 Feb Jobs: Labor market weakening

Nonfarm payrolls -92k vs. est. +55 est. & +126k prior

Unemployment rate up to 4.4% from 4.3%

Average hourly earnings +3.8% YoY vs. +3.7% prior

😑 Jan Retail Sales: Volatile categories drove weakness

Headline: -0.2% m/m vs. -0.3% est. & 0% prior

Control group: +0.3% vs. 0% prior

👍 Feb CPI: Flat (but does not reflect oil price spikes)

Headline: +2.4% YoY vs. +2.4% est. & +2.4% prior

Housing costs continue to cool

Core: +2.5% vs. +2.5% est. & +2.5% prior

⏭️ LOOKING FORWARD

Macro:

Coming today

Q4 GDP “second release”. The initial estimate was 1.4%.

Jan PCE, expecting an acceleration to 3.1% from 3.0% YoY

Jan durable goods orders, expecting an acceleration to 1.1% from -1.4%

Jan JOLTS Job Openings

Next week: Feb PPI

Nvidia GTC is next week. I expect this to affect companies in the supply chain based on updates to AI datacenter architecture. Jensen’s keynote is on Monday.

Looking for any major policy response from the Trump administration with respect to oil prices.