Weekly Musing 03.20.26

Energy forever changed, Nvidia raises the bar, lasers

⏮️ LOOKING BACK

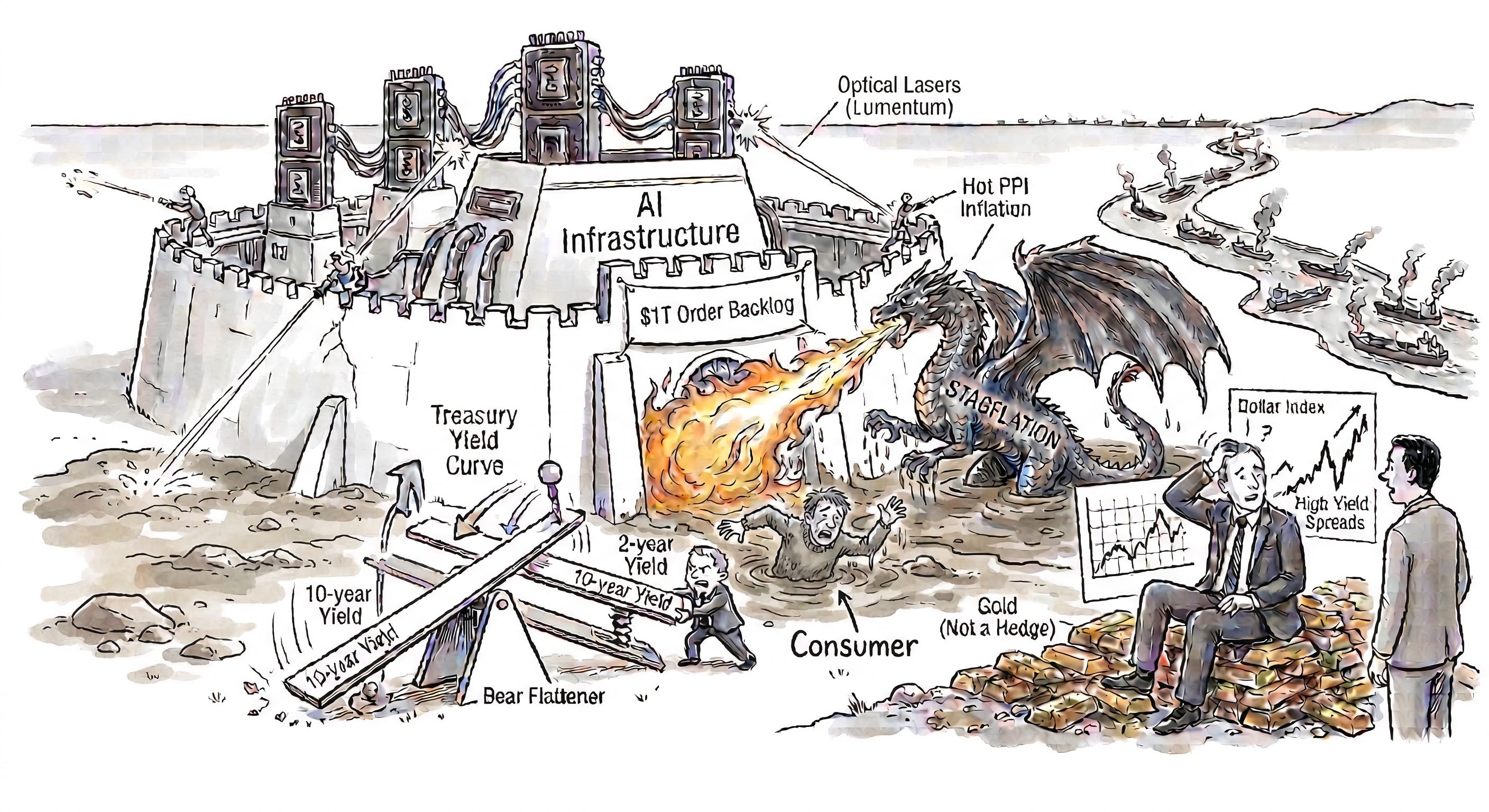

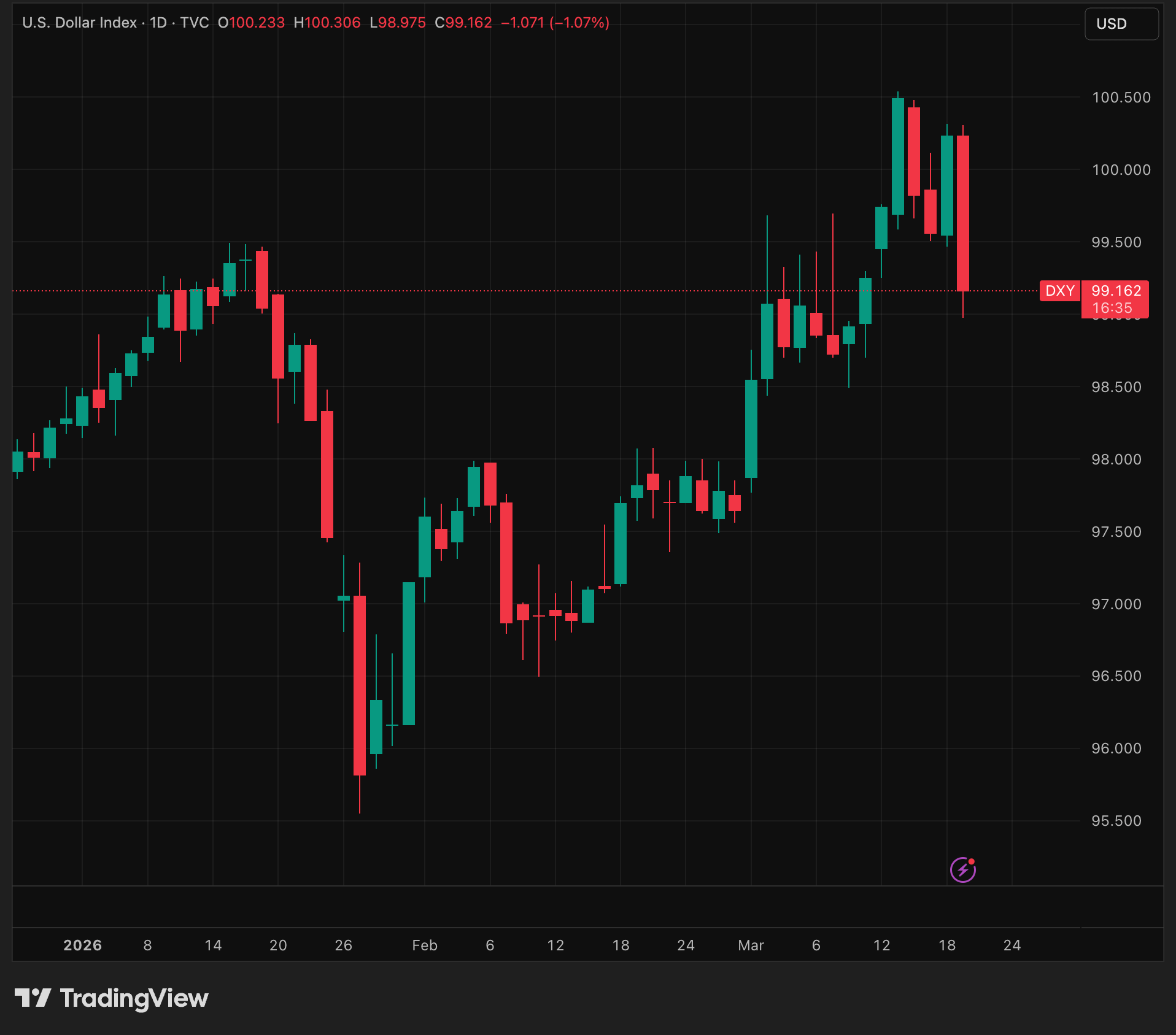

👀 Markets at a Glance

Needless to say, risks are increasing. But over the last few weeks markets largely seem un-phased with lingering optimism (TACO? OBBB tax stimulus? financial deregulation?).

But markets might be finally capitulating.

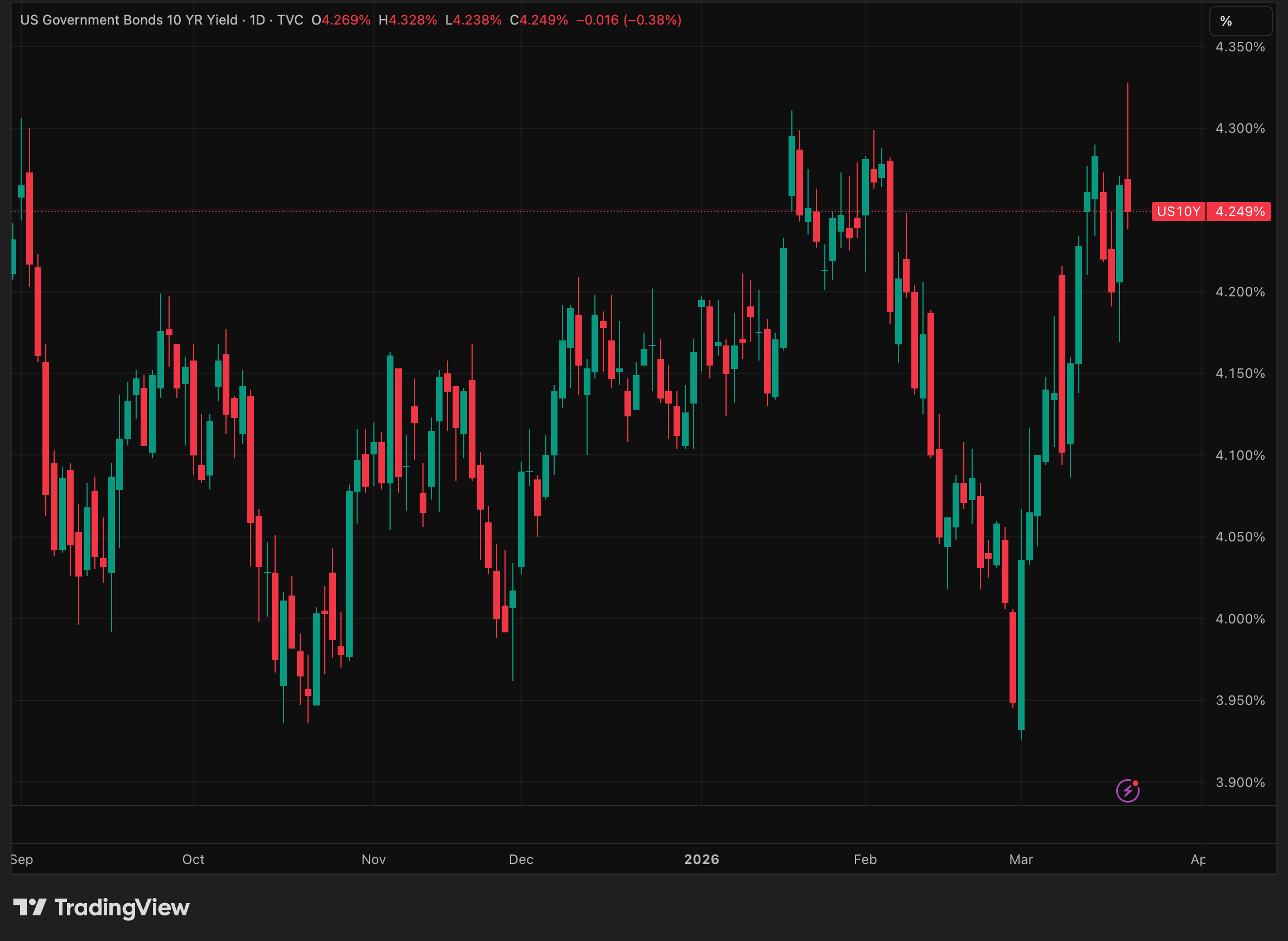

▶️ First, treasuries rates across the curve have been breaking out.

Before the Iran conflict, folks thought rates would decline on softer jobs data and declining inflation. The 10Y hit a 12+ month low below 4%.

Since the Iran conflict began, rates reversed course on inflation concerns.

This week folks are pricing a longer conflict and limited ability for the US to offramp. To make matters worse, wholesale prices (PPI) came very hot.

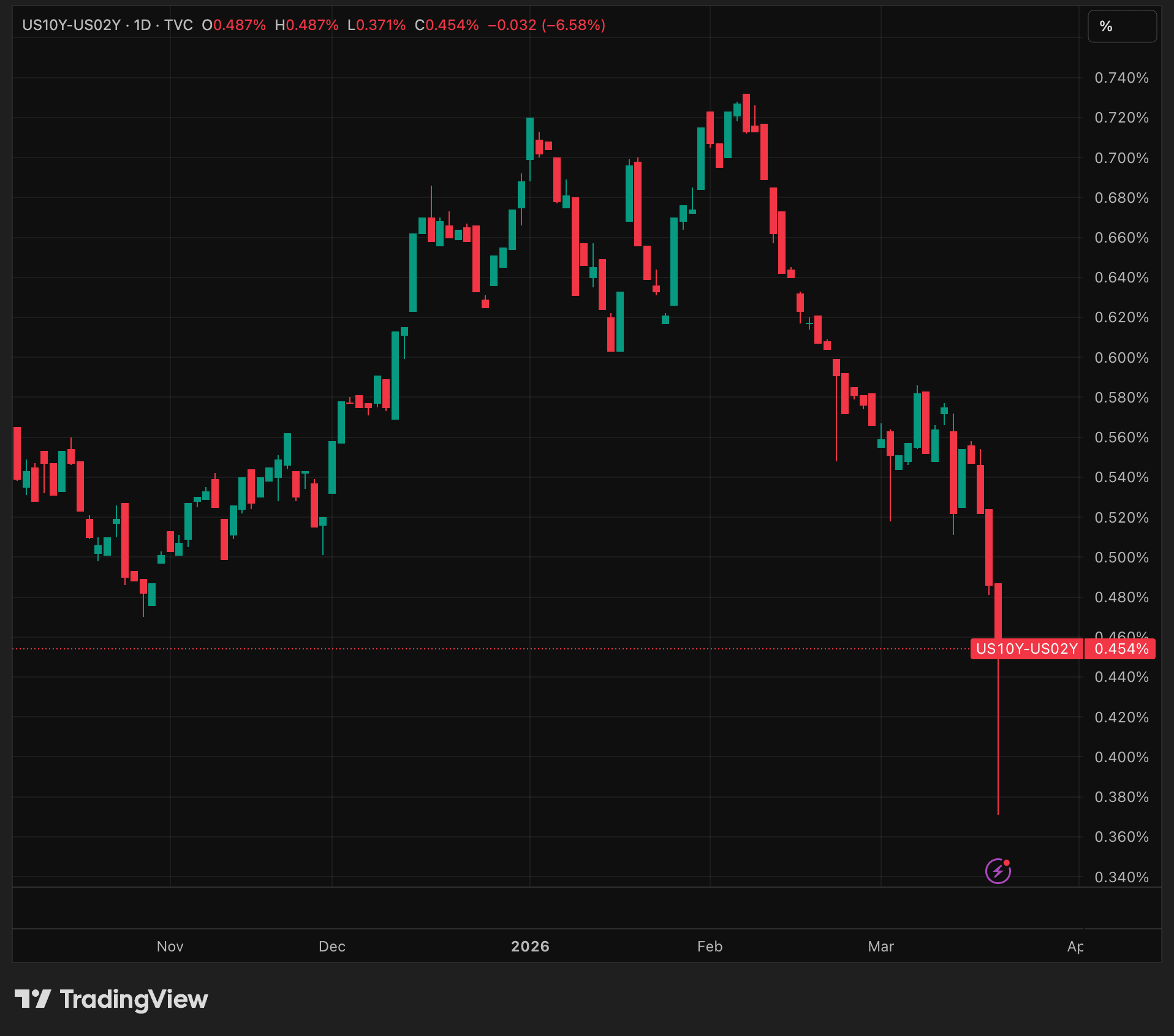

▶️ Further, the 2-year Treasury yield is currently rising faster than the 10-year yield, creating a "bear flattener" in the 2s/10s spread.

The shift signals a tightening credit environment and an increasing risk of stagflation.

With narrower spreads, banks have less profit incentive to lend (because they borrow short and lend long, i.e., net interest margin). This would pull credit out of the economy and negatively affect growth.

Also, if inflation becomes unanchored, we will see destruction in consumer demand. Combined with stagnant growth from credit contraction, we arrive at a stagflation scenario (high inflation + no growth).

The rise in 2Y rates may be bond investors wanting the Fed to act sooner to control inflation.

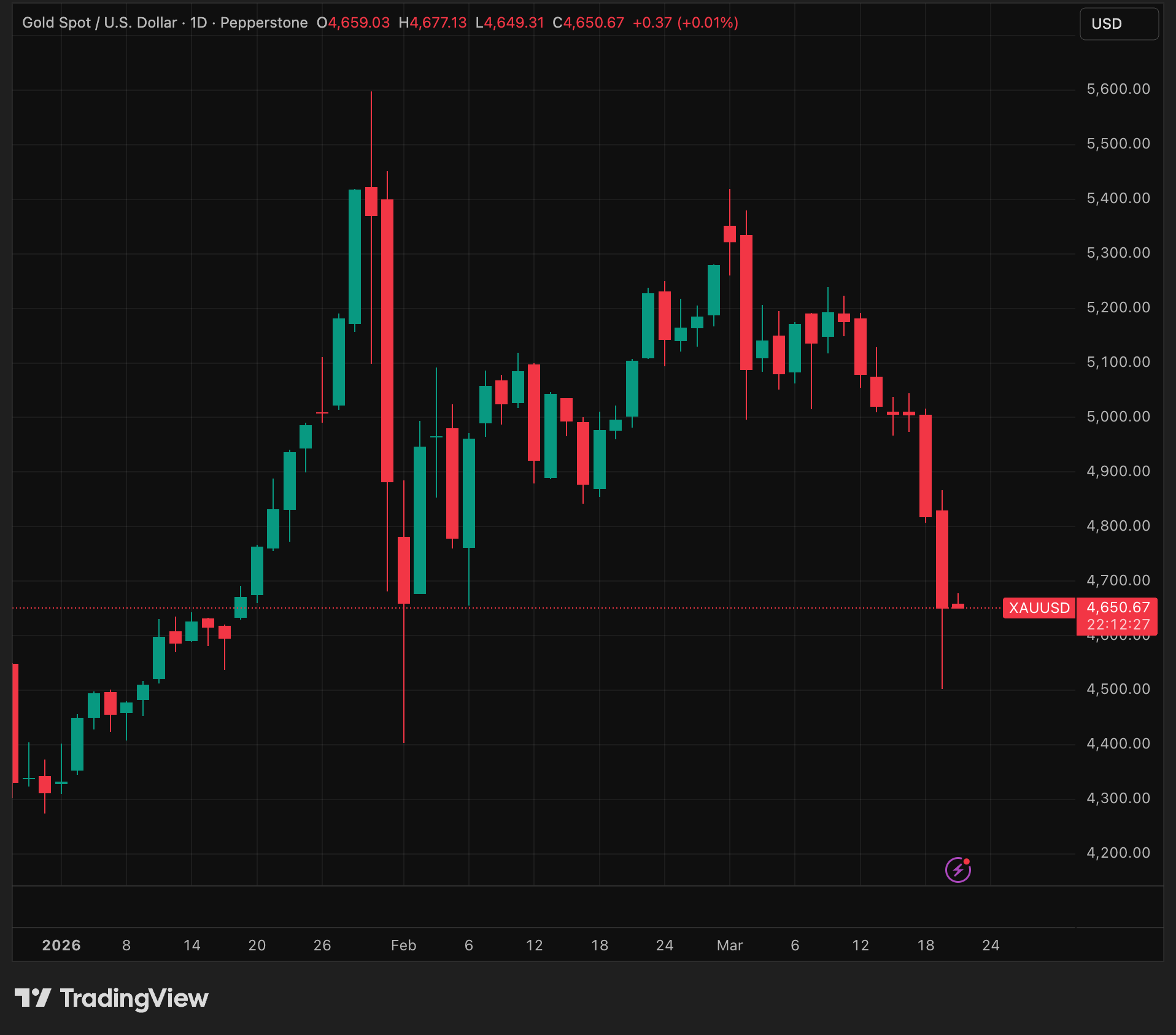

▶️ Next, gold sold off aggressively. Wait, isn’t gold a good inflation hedge? The context matters.

Gold has a huge run up recently attracting a lot of speculative demand.

As treasury rates increase, investors may be tempted to to shift into safe yield bearing and highly liquid US treasuries. A gold selloff anticipate this.

Another contributing factor could be the sudden demand spike for dollars. The price of energy is up a lot, which means countries need more dollars to buy energy and keep their economies running.

Some analysts speculate that we could see broader asset selloffs by Asian and European countries to fund their energy needs.

▶️ Finally, high yield credit spreads (the difference between junk bond interest rates and treasuries) are spiking after historic lows. Junk bonds are being repriced on fears of private credit losses. There is also fear that stagflationary risks put further credit stress on low credit quality corporate borrowers. But spreads have a long way to go before we see real trouble. And when they blow out, it’s usually too late 😅.

Global energy is forever changed

A few key developments this week signal that the conflict in Iran has transitioned from a temporary geopolitical shock to a multi-year structural shift in global energy markets.

60-Day Jones Act waiver: This rare administrative move signals the White House expects prolonged domestic supply friction. By allowing foreign vessels to move SPR releases, the administration is bracing for the Strait of Hormuz to remain a high-risk zone through at least late spring.

Attacks on energy infrastructure: We have moved past the "symbolic" phase of escalation. Previously, strikes targeted storage tanks (downstream), which are easily rebuilt. This week’s strikes targeted upstream capacity. These assets are harder to fix.

Iranian energy infrastructure attacked: Israeli strikes on an Iranian processing hub targeted upstream assets rather than just storage. This knocked out roughly 10-20% of Iran’s gas capacity, hitting the core nerve center of their export ability.

Iran retaliates against Qatar: Iranian retaliatory strikes on Ras Laffan, the world's largest LNG export hub, have knocked out 17% of Qatar’s export capacity. QatarEnergy expects that the damage would take out capacity for 3-5 years while the infrastructure is repaired. The loss of capacity has forced Qata toward 5-year force majeure declarations for major buyers like Italy and South Korea.

My take: I don’t think anyone knows when and how this will all end. But the risks for prolonged energy market disruption are accumulating and hardening. When this does end, countries will surely diversify their energy purchases, which could actually benefit the US (i.e., our energy sector could do well enough to stave off stagflation). Other countries, though, would face a lot more pain. It also may further push these countries to adopt renewables faster (solar, wind, nuclear, battery storage). 🤔

Nvidia raised expectations at GTC

Nvidia hosted their annual conference this week. I am working on a more detailed post covering my top takeaways that the headlines miss + what this means for investing in the AI infra theme.

The biggest headline: Jensen sees $1T+ of orders for Blackwell and Rubin through 2027. The investment community quickly moved to debate what this actually meant (Jensen likes to provide these big splashy numbers without a lot of detail). Management clarified with analysts that the $1T number didn’t include Rubin ultra (2H27), Groq servers, CPU servers, storage solutions, China hopper sales, or any incremental new orders between now and the end of next year. So the $1T is an expectation floor!

So what?

As of this writing, consensus revenue estimate for revenue through 2027 is ~$750-800M, 20-25% below $1T. The highest estimate is ~$975M, slightly below Jensen’s baseline number.

Using consensus estimates, Nvidia trades at 21x NTM P/E, around the same multiple of the S&P 500. If we use the highest analyst estimates, Nvidia trades at 17x NTM P/E.

But that stock has been pretty much dead money for the last 6 months. What’s going on here?

My take (not investment advice 😅): The market is overweighting risks (financing, ROI, and energy availability). Plus, these numbers are literally insane. BUT what’s going on right now is unprecedented (Anthropic is adding billions in revenue a week 🤯). And if you look at where this is all going (hint: stay tuned for my GTC write up), it will get even crazier. Sure, the risks I mentioned are valid. But you have to ask yourself: is the juice worth the squeeze at this valuation?

Lasers

Lumentum has had a wild ride up over the last year. I was fortunate to make an investment back in October. Why is this obscure company mooning?

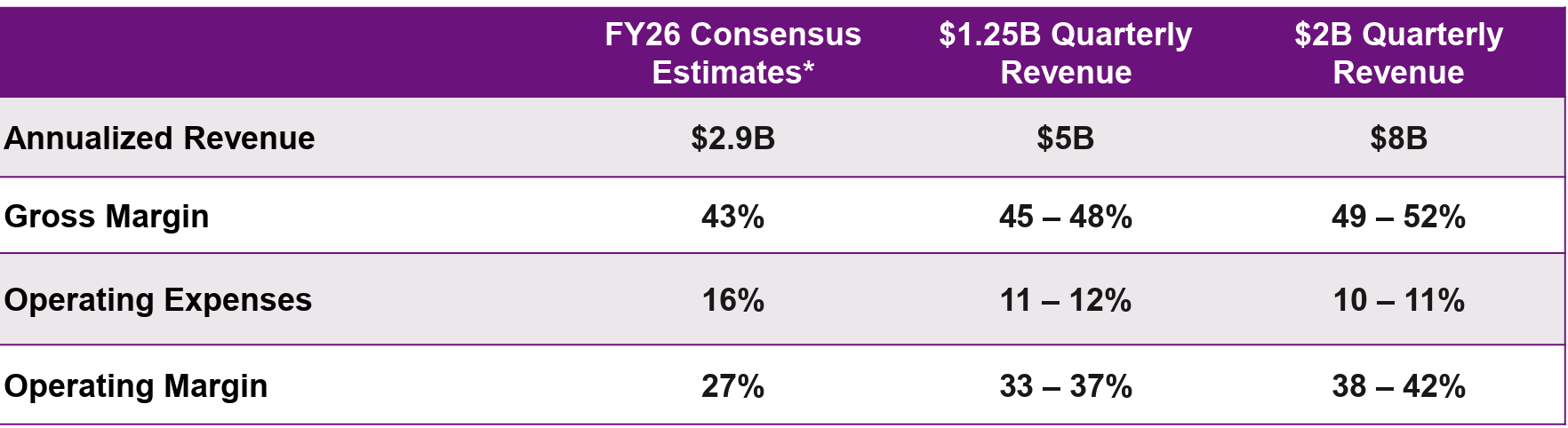

Lumentum is a major vertical integrated optical supplier to the datacenter build out. Optical hardware is an key part of the networking infrastructure in data centers. To satisfy the capex plans by hyperscalers, we will need a way more lasers than the world has capacity to build.

This week, Lumentum’s management provided analysts with a massive update to their guidance, expecting to hit $8B annualized revenue in 18-24 months. This is ~2.5x what they will do in FY26 (ending June). They also expect the optical TAM to grow to $90B by 2030, up from $18B in 2025, representing a 40% CAGR!

There is a lot more to say about Lumentum and the whole optical supply chain (which is getting a lot of attention now). Stay tuned.

Macro: Q4 GDP revised down, PPI blazing hot

🛑 Q4 GDP (2nd release): Disappointing with revisions downwards across every category

+0.7% QoQ ann., revised down from +1.4%

Downward revisions driven by exports, government spending, and consumer spending

👍 Jan PCE

Headline: +2.8% YoY vs. +2.9% est. & +2.9% prior

Core: +3.1% YoY vs. +3.1% est. & +3.0% prior

😑 Jan durable goods orders: Improvement but lower than expected

+0% MoM vs. +1.2% est. & -0.9% prior

👍 Jan JOLTS: Improvement overall, but still trending down over last 6 months

6.95M vs. 6.7M est & 6.55 prior

🥵 Feb PPI (wholesale prices): Blazing hot

+0.7% MoM vs. +0.3% est. & +0.5% prior.

Feels like there is some nuance—mix of tariff and seasonal impacts

Biggest drivers:

Food - weather related issues for produce

Energy - pre-Iran impact, could be in anticipation of conflict

Services saw 10th consecutive rise in prices.

Trade margin (profit margin charged by wholesalers) has been rising rapidly over the last few notes

⏭️ LOOKING FORWARD

Macro: Slow week, but notable will be consumer confidence survey data

SPY and QQQ are testing key support levels. A failure to keep above the 200 day moving average could spell a deeper selloff.

I’m also looking at bitcoin, which is trying to stay above it's 50 day moving average. It would be a battle, but a small step in potentially a start to reversing a deeply negative trend.

We are coming up on 3 weeks for the Iran war. We heard some mixed signals from Israel yesterday (offering help to open Hormuz, but also possibility of ground troops). We will need to start hearing about credible off ramps soon.

MY PORTFOLIO SNAPSHOT

This past week, I’ve been torn between two perspectives: intense optimism regarding AI and growing concern over macroeconomic risks. Here is what I’m thinking.