Weekly Musing 03.30.26

Stagflation risks? Another DeepSeek-like scare. GPU rental prices higher. An anti-climatic end to the Iran war 🤞

Every time we have violent selloff, I watch this video for a dose of resolve.

This week:

Do we have to worry about stagflation? Bond markets don’t think so, not yet.

High treasury volatility may signal more TACOs

Google TurboQuant scaring investors like DeepSeek 2025

GPU rental prices inflecting higher (what bubble?)

Iran conflict end might be anti-climatic 😅

📊 Markets at a Glance

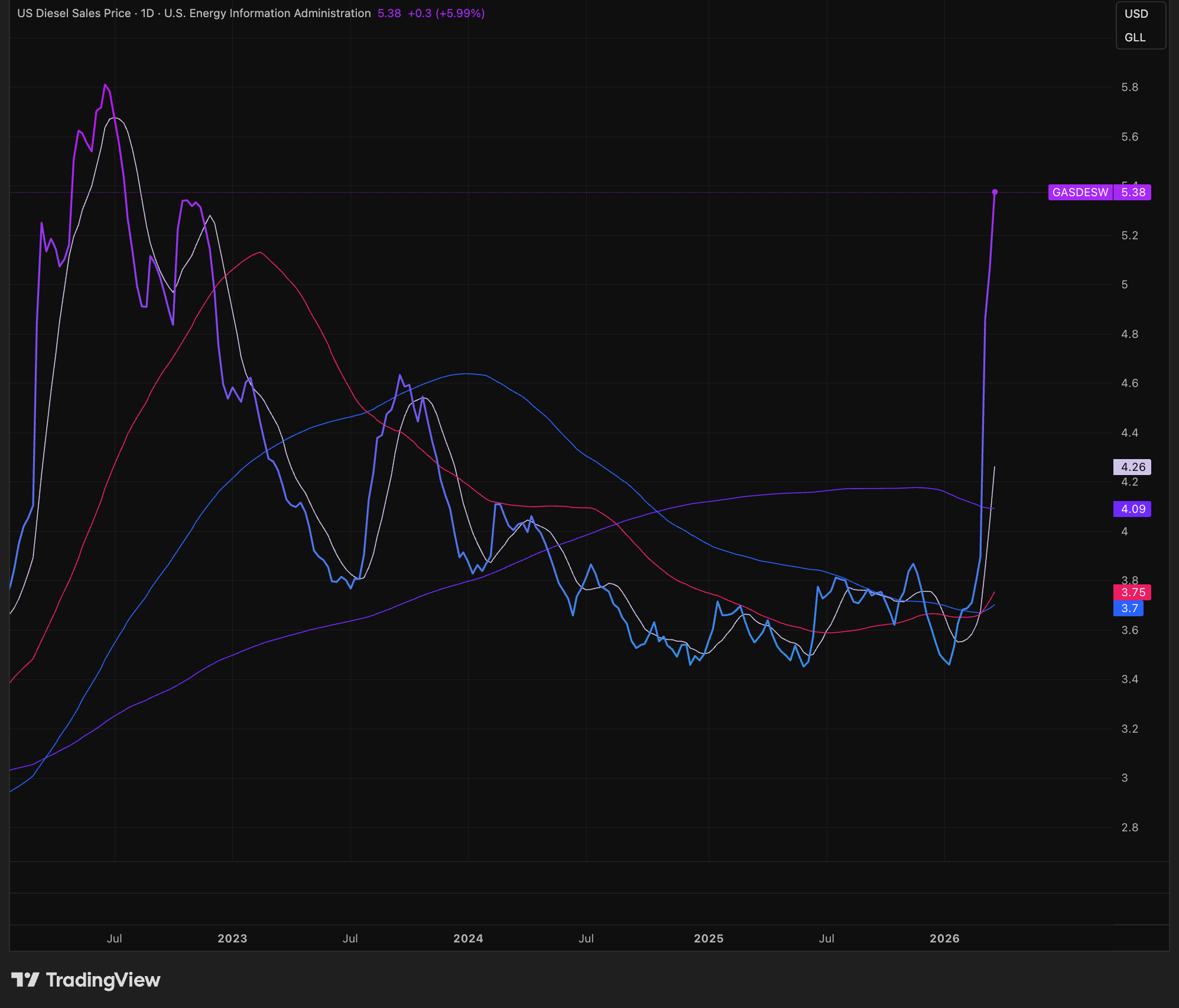

Energy prices whiplash…stagflation?

Oil prices have been super jittery on headlines, making it hard to extract a long-term signal. To make matters worse, domestic diesel prices are increasing rapidly, which adds to the list of inflationary risks (the transportation of goods depends on diesel).

That whiplash is reverberating throughout the rest of the market (what a bloodbath!). Stagflation would be terrible for equities. Are folks worried?

…but bond markets might be telling another story

Bond markets are much more intentional and is where smart money plays. The smart money is downplaying stagflation risk. Stagflation is marked by persistent inflation and low growth. But the market pricing doesn’t reflect this.

First, some background. The Fed monitors market based signals to gauge how investors are pricing inflation over the next 10 years.

Short-term inflation expectations over the next 5 years (T5YIE).

Long-term inflation expectations from year 5 to 10 (excludes the next 5 years (T5YIFR).

What do bond markets say? The inflation shock will be temporary / not persistent.

Next 5 years, inflation expectations are increasing (measure: T5YIE up).

Year 5-10, inflation expectations are decreasing (measure: T5YIFR down)

…meaning long-term inflation is well anchored (not runaway).

Important note: this is what the bond market thinks today, but volatility is elevated so things could change.

Rising 10Y real yields further demonstrate low stagflationary risk. Real yields reflects how much interest the government pays above inflation. With stagflation, we would see real yields decline (i.e., low growth - high inflation).

Treasury volatility is spking.

The MOVE index measures treasury yield volatility. Wall Street monitors this closely — the liberation day MOVE spike gave birth to the first TACO.

⏮️ LOOKING BACK

🧠 Google's TurboQuant shook memory stocks

Google released a breakthrough in inference architecture. I’ll have Claude explain the details. The upshot: another model efficiency improvement.

The market's immediate read: memory is going to be less important. Memory stocks got hit, with Micron and Sandisk selling off ~20%. Interestingly, SK Hynix (Korean-listed memory supplier) didn’t panic. The Koreans are less convinced this is a memory killer. And I think they’re right.

This is deja vu — Deepseek all over again. TurboQuant is a continuation of a long trend already. Models are getting more efficient and will continue! Cue our friend Jevon.

For those who need a refresher: Jevons Paradox states that when a resource becomes more efficient to use, total consumption of that resource tends to increase, not decrease. More efficient models lower the cost of running inference, which drives more use, which drives more compute and memory demand. Efficiency expand the addressable market.

Also, in a post from last week, I said that hardware capability is going to get so much better in the next few years that models are going to become way bigger. They will need all the memory efficiency they can get!

Case-in-point: Leaks of Anthropic’s next generation model spread like wildfire today. Mythos, a new tier above Opus (most capable model today), is a step change. Rumors are floating that Anthropic (in typical fashion) is holding back the model because it’s really good at hacking. They wanted to give the cybersecurity industry a first look so they can be prepared. Scary stuff.

My take: Needless to say, I think this is bullish for memory. I'm genuinely astonished at how consistently markets underestimate the ceiling on intelligence.

⚡ GPU Rental Prices Are Spiking…hard

The older Hopper generation (H100) is seeing prices continue to rise since December. Blackwell (the latest Nvidia generation) has seen a recent spike.

Why is this happening? Simple: a sudden demand surge that the infrastructure wasn't ready for. Since December, coding agent adoption has gone through the roof. Demand (digital) pulled forward faster than supply (physical) could respond.

Anthropic is feeling the pinch directly. They're reducing usage limits to accommodate more demand.

A few implications I keep coming back to:

Capacity is a premium. Clouds with large installed capacity serving variable demand or have large pipelines of coming supply will benefit through higher pricing.

Underinvestment risk is real. OpenAI will capitalize on any hesitation by competitors. We're already seeing this dynamic play out. Microsoft was slower to accelerate capex than some peers, and Azure started showing early signs of market share risk. They may have gotten the memo, quickly moving to acquire an abandoned OpenAI/Oracle expansion project in Abilene, TX.

Mustafa Suleyman@mustafasuleymanGreat way to wrap up the week! We’re partnering with Crusoe on a 900MW AI factory in Abilene, Texas. Super excited to add more capacity to our AI fleet. crusoe.ai/resources/news…

Mustafa Suleyman@mustafasuleymanGreat way to wrap up the week! We’re partnering with Crusoe on a 900MW AI factory in Abilene, Texas. Super excited to add more capacity to our AI fleet. crusoe.ai/resources/news… 3:10 PM · Mar 27, 2026 · 10.2K Views24 Replies · 24 Reposts · 167 Likes

3:10 PM · Mar 27, 2026 · 10.2K Views24 Replies · 24 Reposts · 167 Likes

🌍 The US-Iran Pendulum

It was a wild week of escalation and de-escalation, all within the same news cycle. You can see it in the oil swings and in the Treasury vol index referenced above.

The best framing I heard all week came from analyst Michael Every, who made a point that stuck with me: none of us really know anything. Every public statement from both the US and Iran should be treated as a signal designed to mislead, not inform. Neither side has any incentive to reveal true intentions. The information environment is adversarial by design.

That said, a few things worth noting. The political cost of this conflict is becoming too large in a midterm election year for the US side. Any resolution may come as an anti-climatic de-escalation back to the pre-war status quo.

Though the short term is very hard to predict, the long term may not be: the world is forever changed.

Europe and Asia's energy vulnerability is now undeniable. Asia and Europe are extraordinarily exposed, dependent on Middle East supply. The chart below is emblematic of the problem.

And, though “energy indpendent,” the US is still vulnerable to global supply shocks.

Two implications:

1. US natural gas wins

Asia and Europe will quickly diversify their natural gas supply towards the US. Ever since the Russian-Ukraine war started, Europe has stepped up its supply from the US to replace Russian natural gas. This trend will continue.

The US has a lot of natural gas, but it’s trapped within our borders because transporting requires specialized infrastructure — pipelines, liquefaction, export terminals, etc. The US is investing aggressively to expand export capacity.

The structural export tailwind is on top of two others:

Natural gas is the path of least resistance for AI datacenters as operators are choosing quicker behind-the-meter solutions vs. facing push back/delays getting grid power.

Electrification is a huge tailwind for natural gas. I think we’ll see a renewed push, but not because of climate change. It will be driven by the cost effectiveness for consumers (feels good to own an EV right now!). Natural gas, though a fossil fuel, will become increasingly more important for electrification.

I was talking to a friend in the oil and gas industry this week. The industry understands these trends and is investing in a natural gas future.

2. Return of Nuclear

Nuclear has made a huge comeback in the US as folks started calculating how much power we need for data centers. This realization drove nuclear stocks into a speculative frenzy, pricing in outcomes way out in the future.

But nuclear won’t just be a US trend. I think Asia and Europe will push hard into building new capacity. It’s the only way they can achieve more energy independence and avoid the helpless situation they are in right now.

The nuclear supply chain is similar to that of semiconductors — concentrated, capex intensive, and slow to ramp. We’ll probably see bottlenecks emerge.

One worth watching is HALEU (High-Assay Low-Enriched Uranium), which is needed for new reactor technology (like SMRs). It requires higher enrichment than conventional reactor fuel. Russia is the largest producer of HALEU. We produce very little.

The Department of Energy did two things recently that acknowledge the strategic importance of HALEU.

They began converting weapons grade uranium (from our stockpiles) to HALEU

They invested $1.8B into domestic enrichment capacity.

Both are positive signals, but the supply chain build-out takes time. I think we could see the same types of supply/demand imbalances we are seeing in semiconductors.