Weekly Musing 04.05.26

Sunday night bond market sounding alarm?, small LLM breakthroughs, strong economic data

This week:

Early read from bond markets on Sunday night points to concern

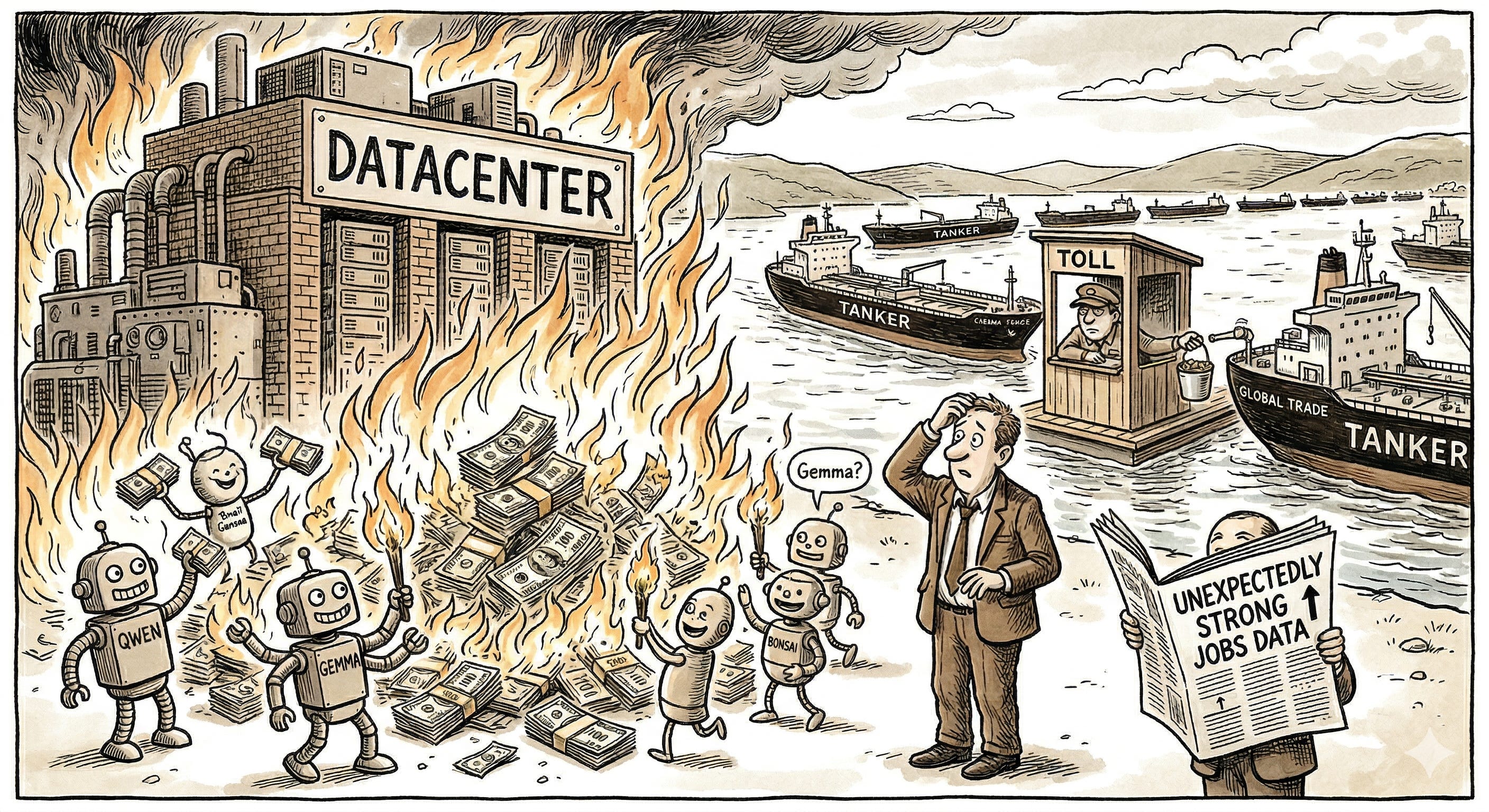

Small LLMs make a leap. Did we just waste a bunch of money on data centers?

A bunch of economic data suprised to

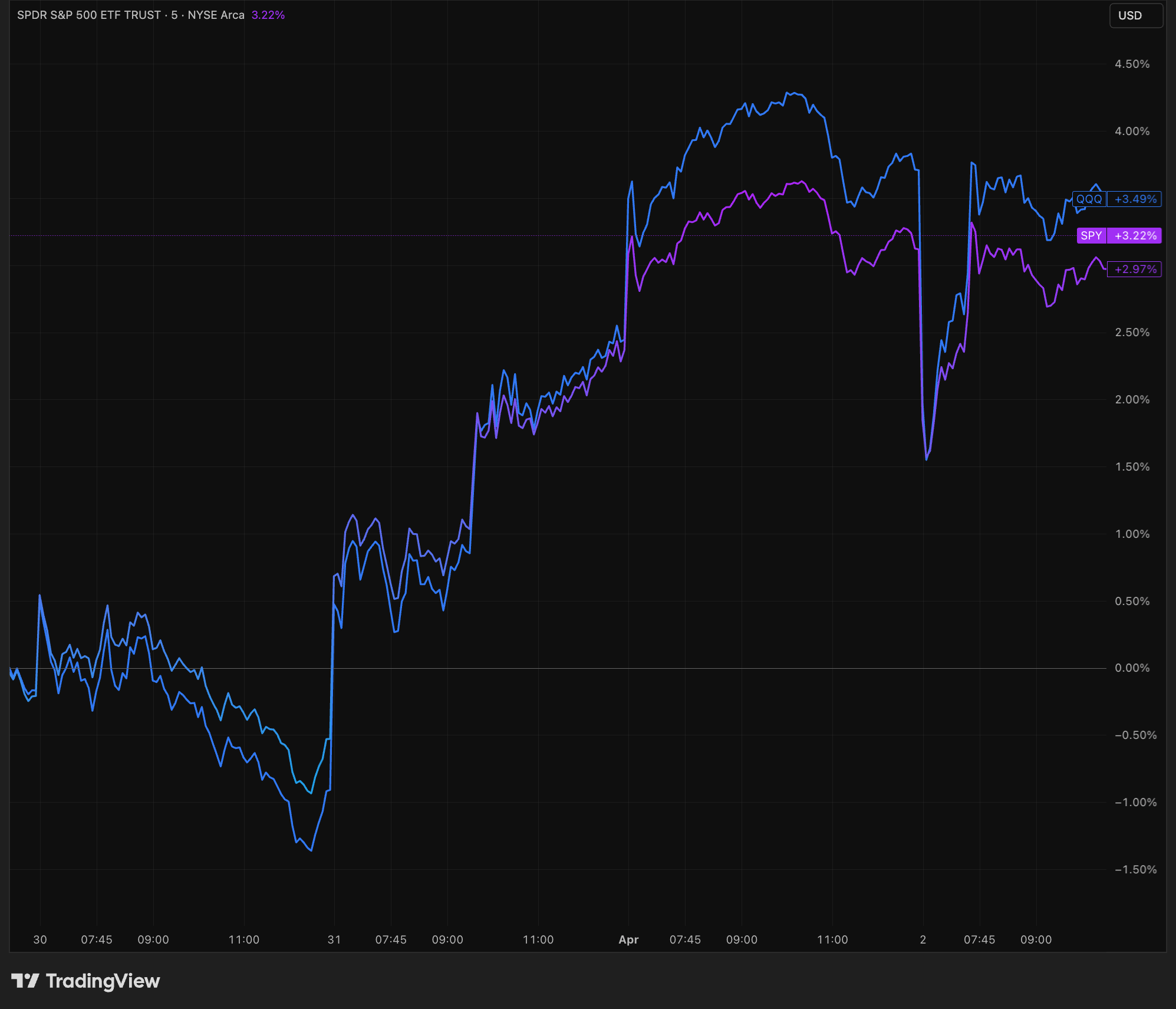

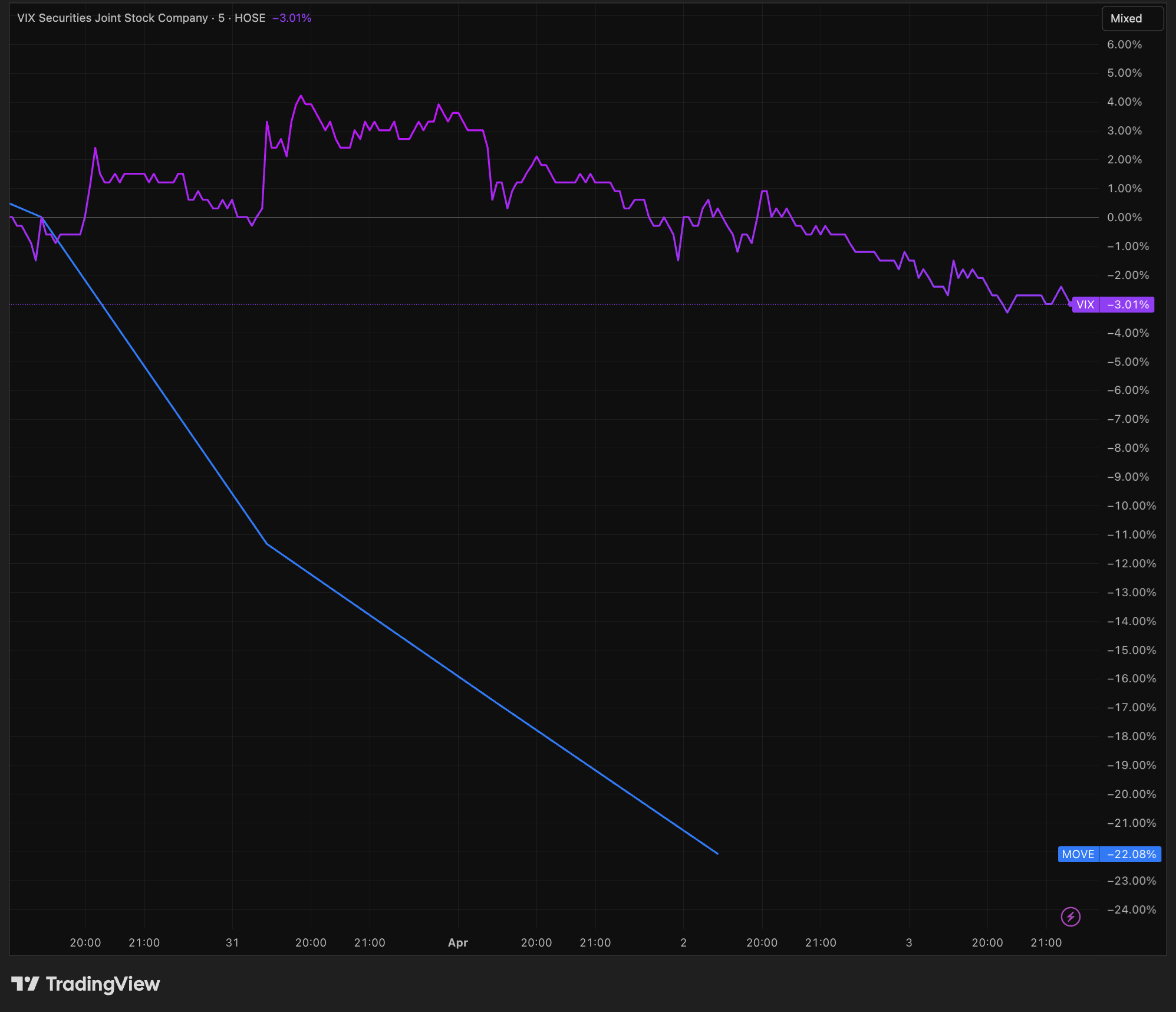

📊 Markets at a Glance

This was another weird, headline fueled week. It felt like there was some serious FOMO for a “face-ripping” rally ahead of an anticipated (magical?) resolution to the Iran conflict and related energy market stress.

Through the end of last week, QQQ and SPY were both up.

And both the VIX (fear index) and MOVE (bond volatility index) were down (bullish).

Treasuries also rallied (i.e., rates were going down)…

…until Sunday night (at the time of this writing). Yields are up meaningfully, hinting at concern.

What’s happening?

It appears Iran is jockeying to be the toll operator for the Strait of Hormuz. Read Citrini’s latest article, it’s a masterpiece. TL;DR, they sent an analyst to Hormuz to witness the situation firsthand. Capitalism at work! They confirmed Iran is facilitating safe passage for ships that play ball.

Hard to believe that the White House would be ok with this. For more than a week, the US military has been fortifying their position in the middle east to escalate. But Trump, once again, pushed back the deal deadline slated to expire today.

Can there be a deal? Who the hell knows. Experts are all over the place. There is a ton of chaos and no one really understands what’s going on.

Seems like bond markets don’t like the outlook as of tonight.

⏮️ LOOKING BACK

🧠 Small models, big brains

In the span of a few weeks, we got three major releases for families of small LLMs—Google’s Gemma 4, Alibaba’s Qwen 3.5, and PrismML’s Bonsai. The largest of these small models (~30B parameters) performed nearly as well on certain benchmarks as their much larger SOTA siblings (trillions+ parameters). The smallest of the models are a few billion parameters and could run on the latest iPhone. Intelligence density has drastically increased (i.e., amount of intelligence per model parameter). Oh, and these small models are all open source!

The latest small models achieve frontier-class performance through a range of innovations — very sparse activation, compression into less bits (quantization), or more efficient information processing. The result is dramatically less compute, memory, or both required per token, without giving up a proportional amount of performance. Larger variants can potentially run on your computer and smaller ones on your phone!

What can they do? The big unlock is that they can reason, are multimodal, and can start to do some agentic stuff…all offline.

Gemma 26B MoE can reason through some code to find a bug, extract some insights from a pdf report, and monitor and react to changes in a system.

Qwen 3.5 9B can help a student study for an exam by summarizing and quizzing on key concepts, help customer service triage tickets, and summarize your e-mail inbox for the day.

Gemma 4 E2B/E4B, the smallest Gemma models, can do language translation and speech recognition.

PrismML Bonsai 1.7B is designed to run on your phone and can summarize your group chat and organize your notes.

Head for the hills, and sell every thing AI infrastructure! It’s all going to burn to the ground.

Kidding. But there are some pretty big implications:

More cloud capacity to do high value things. Counterintuitively, this is good for AI clouds and large model providers. They would love to offload low value stuff to smaller, local models. It improves their unit economics by allocating more of their expensive capacity to high value workloads. Small models will take on some of the basic intelligence / smaller context items and larger models will do the big brain, large context things. They will even work together in some way. Small models will always be on without incremental cost and automatically call on larger models when needed. This might actually drive more cloud AI usage.

Personal computing boom. When I was a kid in the 90s, I paid attention to all the latest PC hardware improvements coming out every year (remember pentium 3?). That made sense back then because we were at the beginning of the internet age. But over the last one or two decades, who cares? Most of the world really didn’t benefit from more capable hardware. That’s going to change. Though these local models are incredibly efficient, they still need more compute and memory than what’s on your personal device today. For the most impressive of the small models, your mac would need 36-48GB of unified memory and the latest Apple silicon for decent speeds and leave enough horsepower to do other things. The majority of computers do not have this. We are going to see a massive upgrade cycle in personal computers and will need a lot more memory. It’s going to be tricky, though. Datacenters are sucking up all the memory supply, making memory for personal devices way more expensive. Apple is trying to bundle their way out of this problem. I just bought a new macbook and the only way I could get more memory was to upgrade to the the next tier of Apple chip. 😅

The edge will get smarter. Siri will get much better this year. I’m confident this will happen. And Apple will do this mostly on device and offline (yay privacy!). But your phone is not the only thing that will get smarter. Anything that requires extremely low latency, high frequency, or needs to be air-gapped and private would benefit — manufacturing anomaly detection, real-time inventory capture for retail, intake patients at a hospital.

🌍 Macro: String of good data

March unemployment rate down (surprised everyone)

Nonfarm payrolls +178k vs. est. +65k & -133k in prior month (revised down from -92k).

This was the best month since December 2024, though it will probably get revised down later.

Strength was pretty broad based across leisure/hospitality, construction, transportation, manufacturing.

Unemployment rate 4.3%, down from 4.4%

Feb. retail sales was higher than expected

Retail sales +0.6% MoM vs. est. +0.5% & -0.1% prior month

Honestly, this has been all over the place in the last several months, so hard to see a trend so far.

March mfg. PMI survey was strong, showing positive trend

Manufacturing PMI 52.7 vs. est. 52.3 & 52.4 prior month

Third consecutive month above 50 (expansionary).

We are seeing signs of optimism for domestic manufacturing after a long period of pessimism.